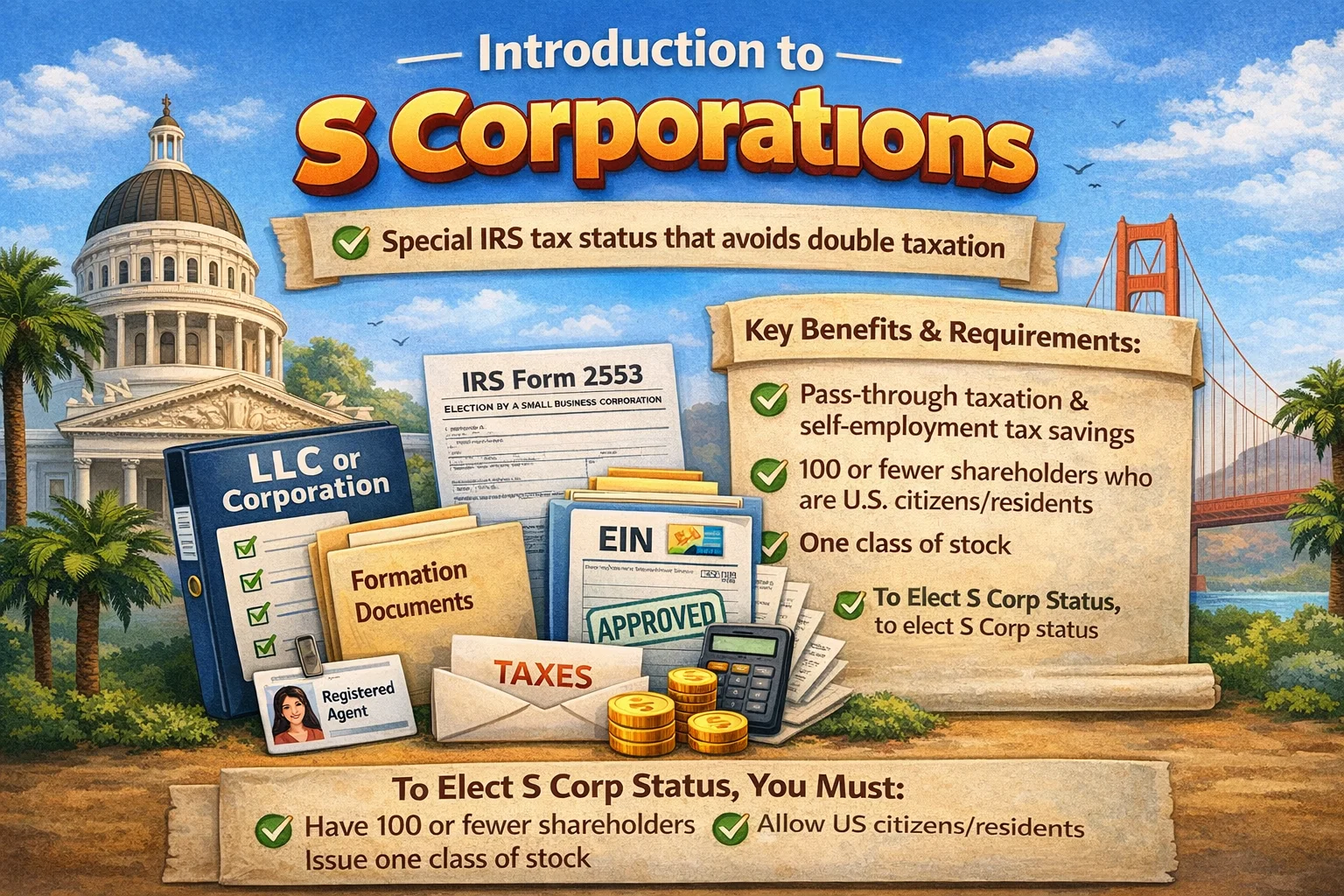

1. Introduction to S Corporations in Connecticut

An S Corporation (commonly called an S Corp) is a special tax status

granted by the

Internal Revenue Service (IRS) that allows eligible businesses to pass income, losses,

deductions,

and credits directly to shareholders for federal tax purposes. In Connecticut, an S Corp

is not a

separate legal entity type but a tax election made after forming a corporation or LLC.

To operate as an S Corp in Connecticut, a business must first be legally formed with the

Connecticut

Secretary of the State and then file

IRS Form 2553 to elect S Corporation

status. Once approved, the business remains subject to both federal S Corp rules and

Connecticut

state tax and compliance requirements.

2. Benefits of Starting an S Corp in Connecticut

Starting an S Corporation in Connecticut can offer significant tax and operational advantages for eligible businesses. While the company must still comply with Connecticut corporate and tax rules, S Corp status is commonly chosen by business owners looking to optimize taxation while maintaining liability protection and professional credibility.

Key benefits of forming an S Corp in Connecticut

- Pass-through taxation: Business income and losses pass directly to shareholders and are reported on individual tax returns, avoiding federal corporate income tax.

- Potential payroll tax savings: Owners who work in the business can receive part of their income as distributions, which are not subject to self-employment tax (subject to reasonable salary rules).

- Limited liability protection: Shareholders are generally not personally responsible for business debts or legal obligations.

- Improved business credibility: S Corporations are often viewed as more established by banks, vendors, and potential investors.

- Predictable ownership structure: S Corps allow up to 100 shareholders and require a single class of stock, creating clarity in ownership and profit distribution.

3. Eligibility Rules for Connecticut S Corporations

To start and maintain an S Corporation in Connecticut, a business must meet strict eligibility requirements set by the Internal Revenue Service (IRS) and comply with applicable Connecticut regulations. Businesses that fail to meet these requirements may be denied S Corp status or have their election automatically terminated.

Core eligibility requirements for S Corp status

- Domestic entity requirement: the business must be formed in the United States as a corporation or LLC registered with the Connecticut Secretary of the State.

- Shareholder limitations: the S Corp may have no more than 100 shareholders.

- Eligible shareholders only: shareholders must generally be U.S. citizens or resident individuals; most corporations, partnerships, and non-resident owners are not allowed.

- Single class of stock: the business may issue only one class of stock, meaning all shares must have identical rights to distributions and liquidation proceeds.

- Approved business type: certain businesses, such as insurance companies and some financial institutions, are not eligible for S Corporation status.

- Timely IRS election: IRS Form 2553 must be filed and accepted within the required election period.

Meeting all eligibility rules is essential for preserving S Corporation status. If an S Corp violates IRS requirements—such as issuing multiple classes of stock or adding an ineligible shareholder—the IRS may revoke the S Corp election, resulting in higher taxes and compliance complications.

4. Connecticut S Corp Fees & Costs

Connecticut has structured business formation and compliance costs. S Corporations must comply with annual state filing requirements through the Connecticut Secretary of the State and may be subject to the Connecticut Corporation Business Tax, even if the business has limited or no income.

| Service | Remarks | Fee |

|---|---|---|

| Formation Charges | Filed with Connecticut Secretary of the State | $250 (Corporation) $120 (LLC) |

| Registered Agent Service i | By Service Providers | $50 – $150 / year |

| Corporation Business Tax (S Corp) | Filed with Connecticut Department of Revenue Services | Minimum $250 / year (if applicable) |

| Operating Agreement / Bylaws | By Service Providers | $0 – $200 ($0 with FormLLC) |

Why Use a Professional Agent?

- Enhanced privacy for owners

- Compliance and filing reminders

- Reliable handling of legal notices

Using a professional service like FormLLC can help you streamline your Connecticut S Corp formation and EIN process, while ensuring a compliant Operating Agreement or corporate bylaws are included at no extra cost. Register now to get started.

Always look beyond just the “formation price”. The real cost includes annual reports, registered agent renewals, Connecticut Corporation Business Tax filings, payroll compliance, and potential late penalties. A complete setup can prevent costly compliance issues later.

READY TO START YOUR CONNECTICUT S CORP?

Get step-by-step guidance on forming your business, filing IRS Form 2553, and handling Connecticut-specific tax and compliance requirements to start your S Corporation the right way and avoid costly mistakes.

Start My Connecticut S Corp5. Complete Formation Process for a Connecticut S Corp

Starting an S Corporation in Connecticut is a two-step process. First, the business must be legally formed as a corporation or LLC with the Connecticut Secretary of State, Business Services Division. Second, the business must elect S Corporation tax status by filing the required election with the Internal Revenue Service (IRS). Completing each step in the correct order is critical to ensure the S Corp is valid and compliant.

- Form a Connecticut business entity: register a corporation or LLC with the Connecticut Secretary of State, Business Services Division and receive confirmation of formation

- Create internal governing documents: prepare corporate bylaws or an operating agreement outlining ownership, voting rights, and management structure

- Obtain an Employer Identification Number (EIN): apply for an EIN from the IRS to identify the business for tax and payroll purposes

- Issue ownership interests: issue shares (for corporations) or membership interests (for LLCs) and document ownership percentages

- Elect S Corporation status: file IRS Form 2553 within the required timeframe to request S Corp tax treatment

- Register for Connecticut tax accounts: enroll with the appropriate state agencies for payroll, employment, and other applicable taxes

- Open a business bank account: separate personal and business finances by opening a dedicated business bank account

6. Filing IRS Form 2553 for S Corp Status

Filing IRS Form 2553 is required for a Connecticut business to be taxed as an S Corporation. Forming a corporation or LLC with the Connecticut Secretary of State does not automatically grant S Corp tax treatment. The business remains taxed under its default federal classification until the IRS approves the S Corporation election.

What is IRS Form 2553?

IRS Form 2553 is the federal election form used to request S Corporation tax status. Once approved, business income, deductions, losses, and credits pass through to shareholders’ individual tax returns instead of being taxed at the corporate level.

When should Form 2553 be filed?

- New businesses: Within 75 days of formation or the beginning of the tax year

- Existing businesses: By March 15 of the year the election is to take effect

- Late filings: May be accepted if the business qualifies for late-election relief and provides reasonable cause

Key information required

- Legal business name and Employer Identification Number (EIN)

- Date of incorporation or LLC formation

- Shareholder names, addresses, ownership percentages, and signatures

- Chosen tax year (calendar year is most common)

7. Annual Filings and Ongoing Compliance Requirements

After forming a Connecticut S Corporation, you must stay compliant with both the Connecticut Secretary of State and the Connecticut Department of Revenue Services (DRS). Missing filings or deadlines can result in penalties, interest charges, or loss of good standing.

Required Connecticut filings

- Annual Report: Filed yearly with the Connecticut Secretary of State to maintain active status

- Form CT-1120SI: Connecticut S Corporation Information and Composite Income Tax Return filed with the Department of Revenue Services

- State tax payments: Composite income tax and pass-through entity tax payments may apply depending on shareholder structure

Federal requirements

- IRS Form 1120-S: Federal S Corporation tax return

- Schedule K-1: Issued to shareholders

- Payroll filings: Required for shareholder-employees

Corporate maintenance

- Maintain corporate records and governing documents

- Document shareholder and director decisions

- Keep accurate financial and payroll records

- Update registered agent and address information

FormLLC can help manage annual filings, track deadlines, and keep your Connecticut S Corporation compliant year after year.

8. Conclusion

Starting an S Corporation in Connecticut can offer meaningful tax and operational advantages, but only when the business is formed and managed correctly. From entity formation and IRS S Corp election to Connecticut pass-through entity tax obligations, payroll setup, and ongoing compliance, each step plays an important role in long-term success.

By understanding Connecticut-specific requirements and maintaining proper filings each year, business owners can avoid penalties, protect their good standing, and maximize the benefits of S Corp taxation. If you want expert guidance at any stage of the process, FormLLC can help you start and maintain your Connecticut S Corporation with confidence and clarity.

9. Frequently Asked Questions

A Connecticut S Corporation is a business that elects S Corporation tax status with the IRS, allowing profits and losses to pass through to shareholders’ personal tax returns while operating as a corporation or LLC under Connecticut law.

To start an S Corp in Connecticut, you must first form a corporation or LLC with the Connecticut Secretary of State (Business Services Division), obtain an EIN from the IRS, and then file IRS Form 2553 to elect S Corporation tax status.

Yes. Filing IRS Form 2553 is required to be taxed as an S Corporation. Without this election, the business will be taxed under its default federal classification.

Connecticut does not impose a traditional franchise tax on S Corporations. However, S Corporations must file Form CT-1120SI (Connecticut S Corporation and Composite Income Tax Return) and may owe state income tax or pass-through entity tax depending on income and ownership structure.

Yes. Shareholders who actively work in the S Corporation must be paid a reasonable salary that is subject to payroll taxes before taking profit distributions.

Connecticut S Corporations must file an Annual Report with the Connecticut Secretary of State, submit Form CT-1120SI with the Connecticut Department of Revenue Services, and file IRS Form 1120-S at the federal level.

Yes. FormLLC can assist with Connecticut S Corp formation, IRS S Corp election, payroll setup, and ongoing compliance to help you start and manage your business correctly from day one.